New Cases in South Korea, Italy, and Iran

Market Note | 2/24/2020

Financial markets have been especially hard-hit today, with reports of new coronavirus (COVID-19) cases appearing in South Korea, Italy, and Iran. The uncertainty over transmission and fears of a global pandemic—and the resulting slowdown in economic/financial activity—has led to the sharp negative response in risk markets.

Of course, there is still much about the medical side of this that is unknown, related to level of contagion, transmission mechanisms, incubation periods, and development of a vaccine. Commentary on these issues would only be speculation at this point. Financial markets, as we have said many times, can adapt when conditions are certain (even if the news is terrible, prices will sharply discount themselves accordingly). However, higher levels of uncertainty create a wider path of probabilistic outcomes, which make it more difficult to pinpoint what various assets are worth at a single moment. This process of market price discovery is important, and can be thrown off-track temporarily by events like this.

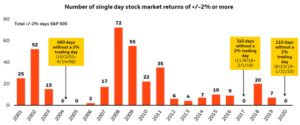

As seen in the chart below, equity market indexes have typically experienced an average of a half-dozen to a dozen or more days per year when prices rise or fall by at least +/- 2%. But, we haven’t experienced such a day since last August, and the last several years have been far less volatile than average. So, we’ve likely become far more sensitive to ‘normal’ market volatility. As in the past, these uncertainties have tended to pass, problems are solved, the current worry moves on to a new one (as global trade fears have moved to this), and human conditions generally improve over time. This results in economic growth, rather than decline, and also explains why risk assets like equities have tended to win more than lose over history.

In the near term, how unpleasant this hiccup becomes is yet to be determined, and perhaps we’ll have to endure more days like this. In a global environment already suffering from slower growth and looking for catalysts for improvement, the timing of a one-off event like a virus is far from optimal. China has already been impacted through quarantines, and by store/factory closures that have a direct impact on shutting down economic activity. If this spreads further, other regions could also be similarly affected. But, at some point, normal business and consumer activity will resume.

The best course, as we believe is always the case, is an adequately diversified asset allocation. It’s an important reminder, that while segments such as bonds do not look exciting from a forward-looking return perspective, especially considering the high correlation between starting bond yields (currently low) and forward-looking multi-year total returns, these prove their worth during times of crisis. Over time, periodic equity ‘resets’ also help keep equity valuations in check, potentially preventing excess exuberance that could eventually result in worse outcomes down the road if the most optimistic predictions prove unsustainable. A skeptical market is likely a healthier one.

Source: Blackrock, as of 1/31/20.